Fabio Baruffa — PhD Quantum Computing · ex-Intel · ex-AWS · Lead Cloud Consultant · Quant Trader & Investor · Startup Mentor

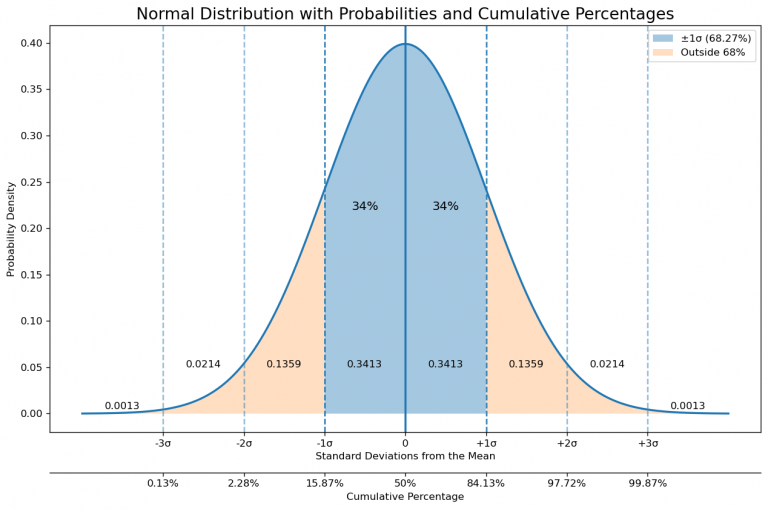

Before earnings, product launches, or Fed announcements, traders face a critical question: How much will this stock actually move? The expected move answers this by...

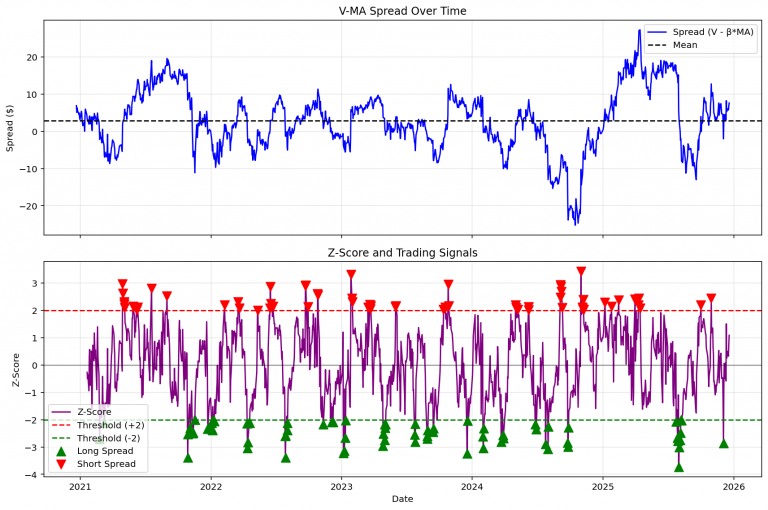

Pairs trading exploits the principle of relative value. Like in physics, we sometimes do not care only about absolute values — we care about deviations from a reference...

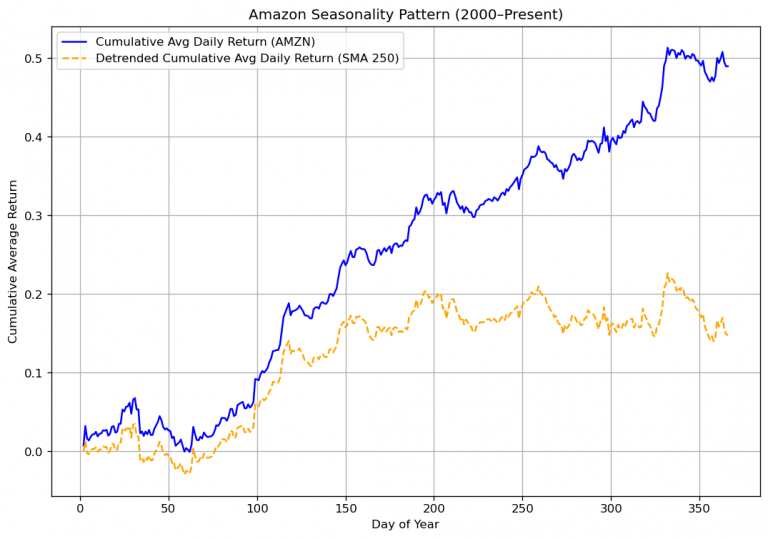

Stock prices — and even their cumulative returns — often show long-term upward or downward trends that can mask underlying behavior.

In this post, we’ll use Python to...

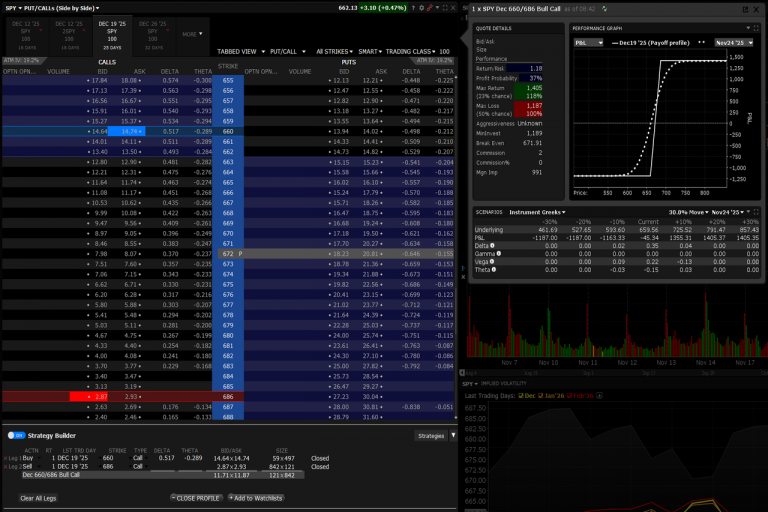

Understanding options data is essential if you want to move from theory to actual, structured trading strategies. Whether you’re tracking implied volatility, evaluating...

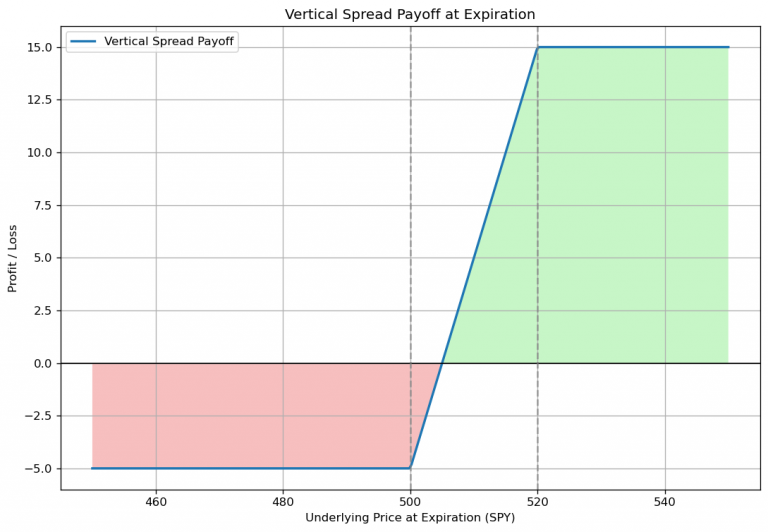

Beyond just seasonal market patterns, learn to trade them using options can give you more flexibility and defined risk...

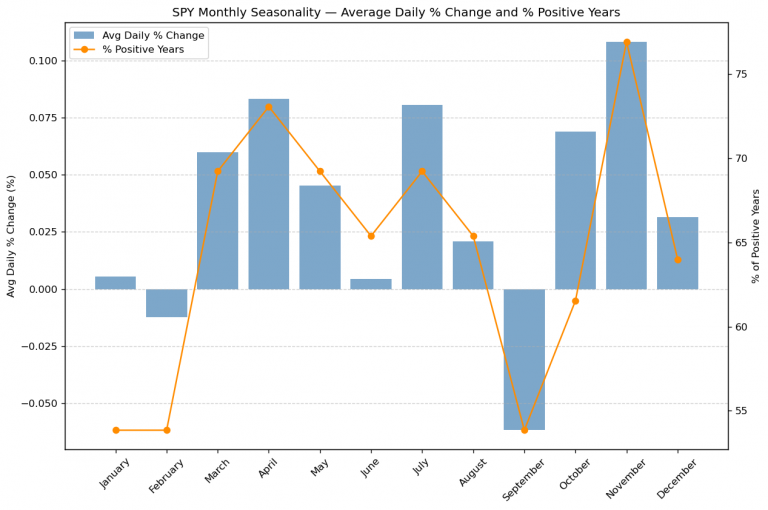

End of year seasonality of the S&P500 ETF (SPY) is one of the most persistent pattern among the seasonal effects study. In this post, I'll take a systematic look at this...