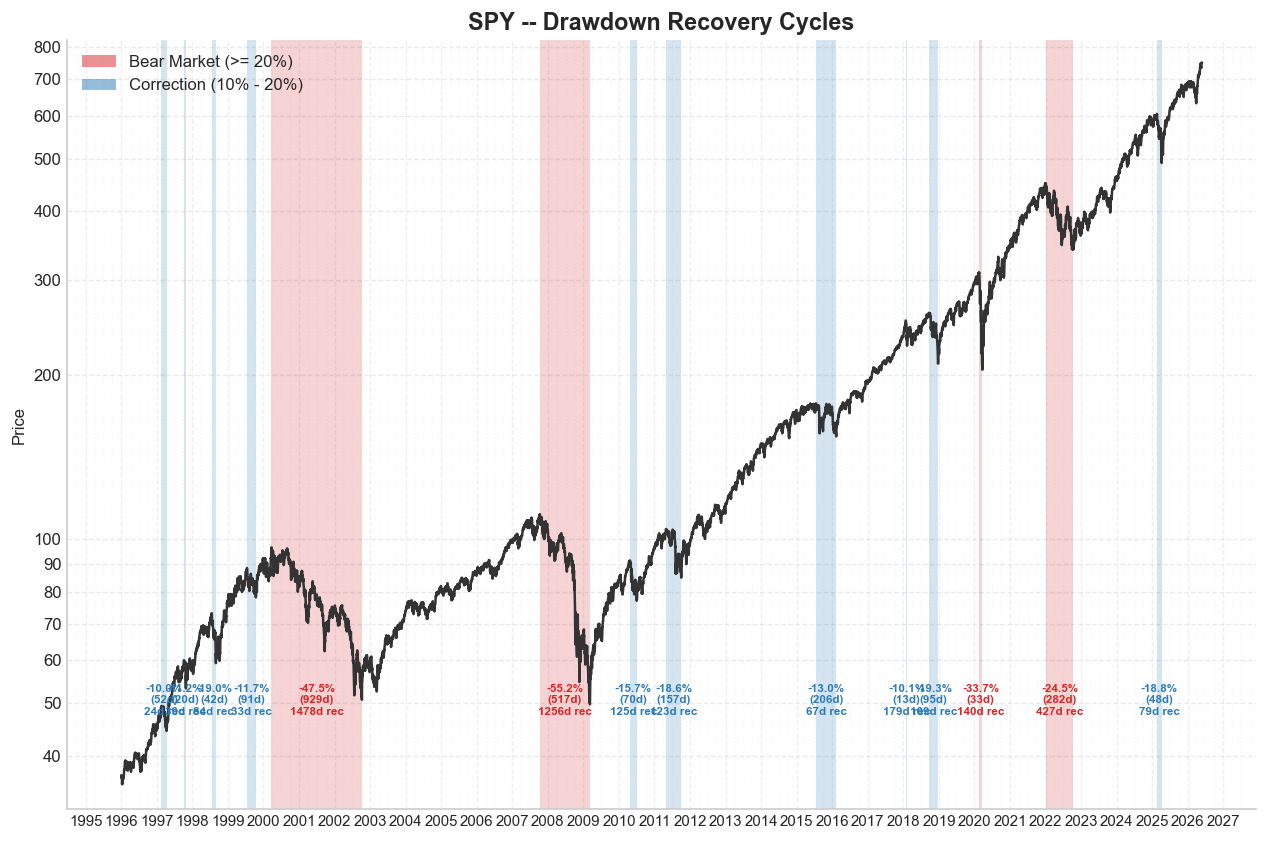

The Anatomy of Bear Markets

Every trader fears the bear market. But how many have actually studied one? I ran a full cycle analysis on SPY, from 1996 to 2026, nearly 30 years and 7,650 trading days. I classified every significant drawdown into bear markets, corrections, and small corrections. Then I measured the duration, the depth, and the recovery time for each one.

0 Comments

May 28, 2026