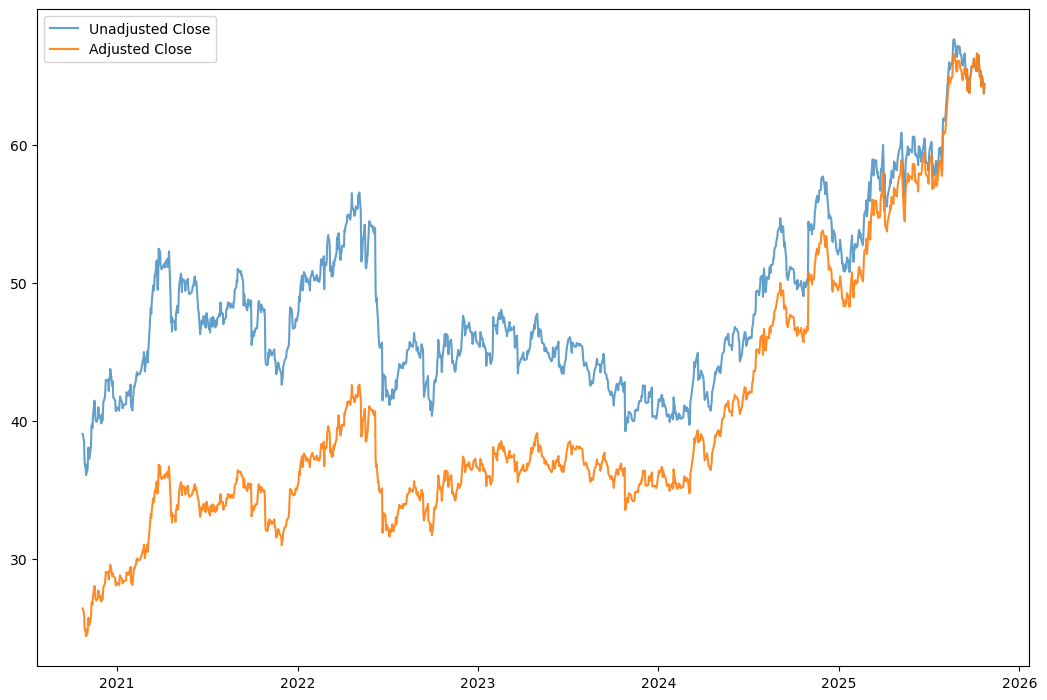

Adjusted vs. Unadjusted Prices: The Hidden Trap

In quantitative trading, like in physics, every model starts with data — and often, that means historical prices. But not all price data is created equal. One of the most overlooked — and misunderstood — aspects of market data is the distinction between adjusted and unadjusted stock prices. It might seem like a small technical detail, but it’s often the difference between a strategy that looks profitable —and one that truly is making money. In this post, I’ll unpack why that distinction matters.

0 Comments

October 19, 2025