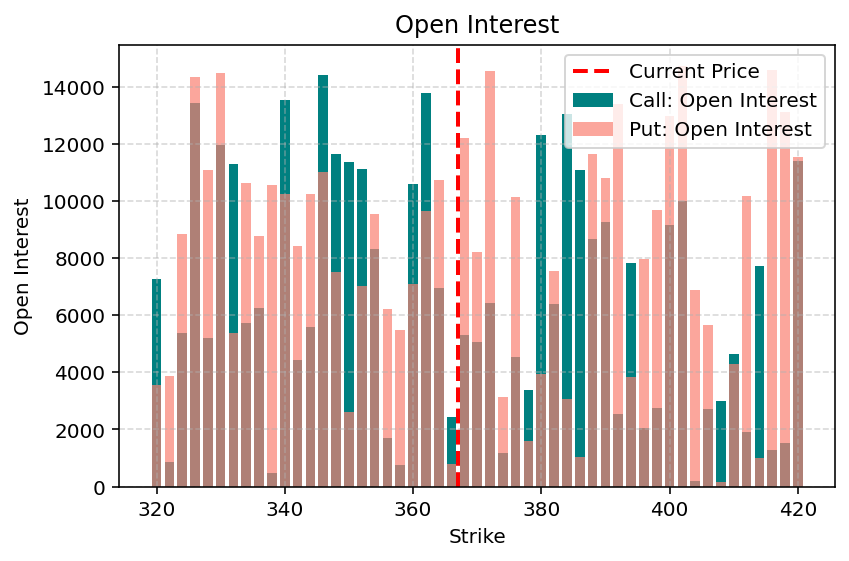

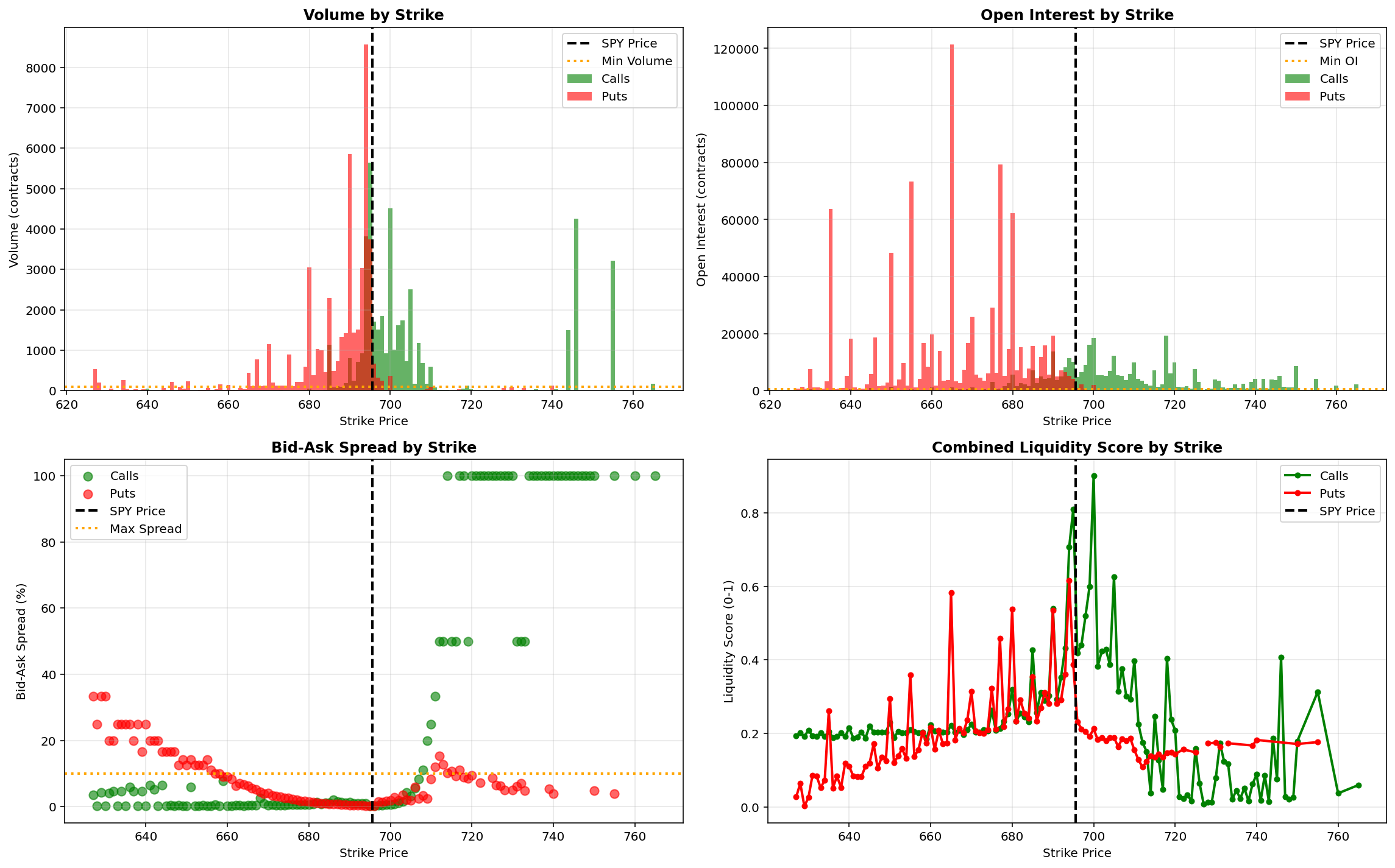

Options Liquidity and Market Execution

Before any option trade, I spend a lot of time analyzing the market, identifying a perfect setup, calculating my edge, and then I enter the trade. My thesis plays out exactly as expected. The stock moves in my favor, and I feel right...But I lose money. How? Liquidity.

0 Comments

January 27, 2026