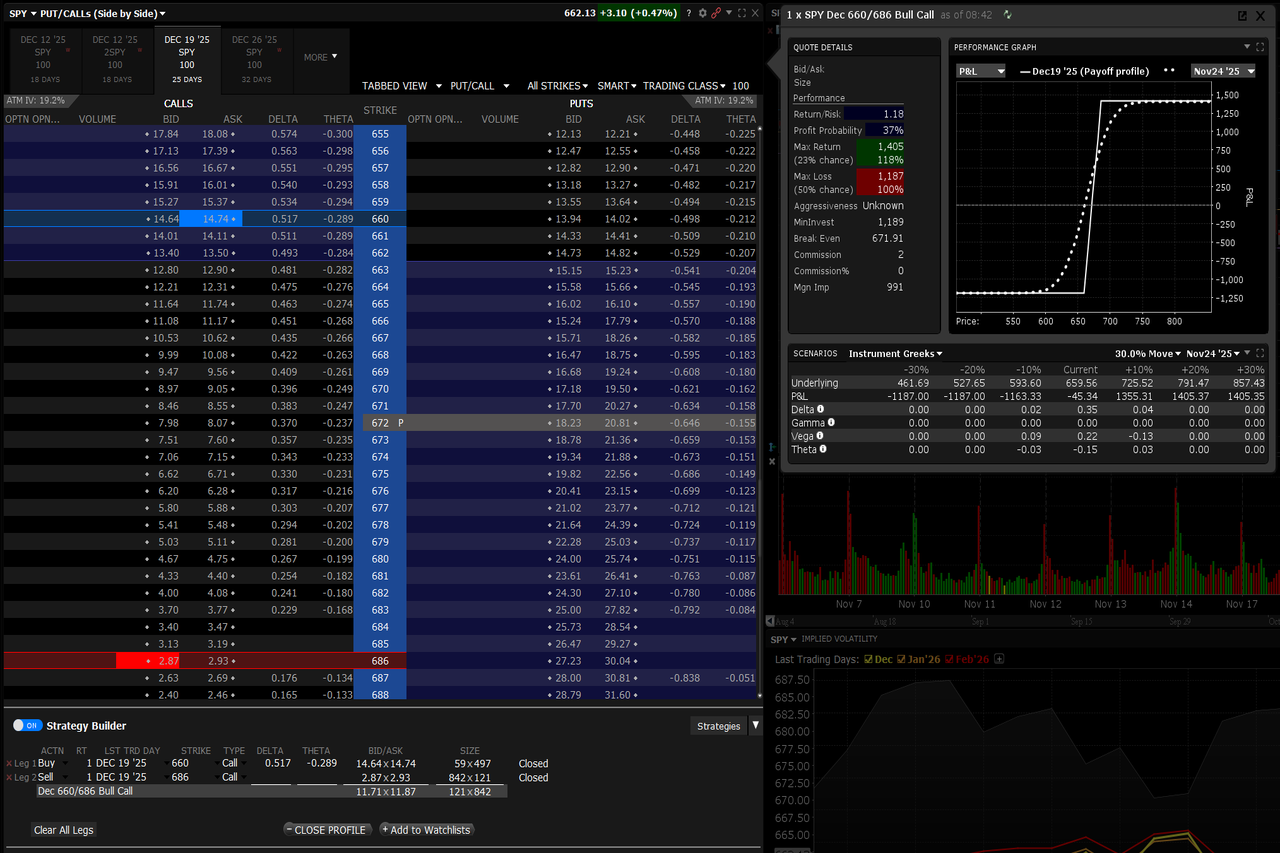

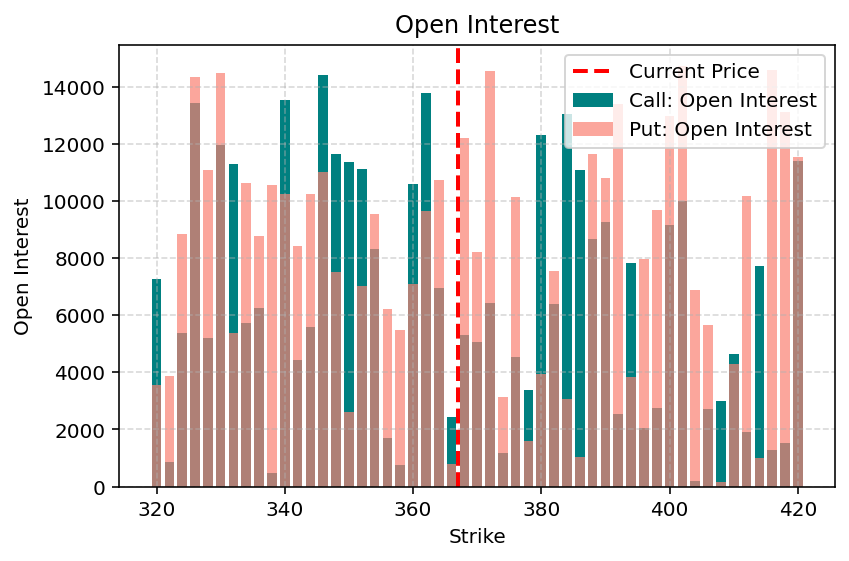

Reading Options Volume and Open Interest

I often find that a simple physics analogy makes trading concepts easier to grasp, particularly when explaining the difference between what’s moving and what’s already there, the flux and the state. The flux measures flow through a surface, like current through a wire. The state describes what exists at a point in time, like charge accumulated in a capacitor. Options markets have a similar duality: volume measures the flow of contracts trading today, while open interest describes the total number of contracts that are still open and exist in the market.

0 Comments

January 16, 2026